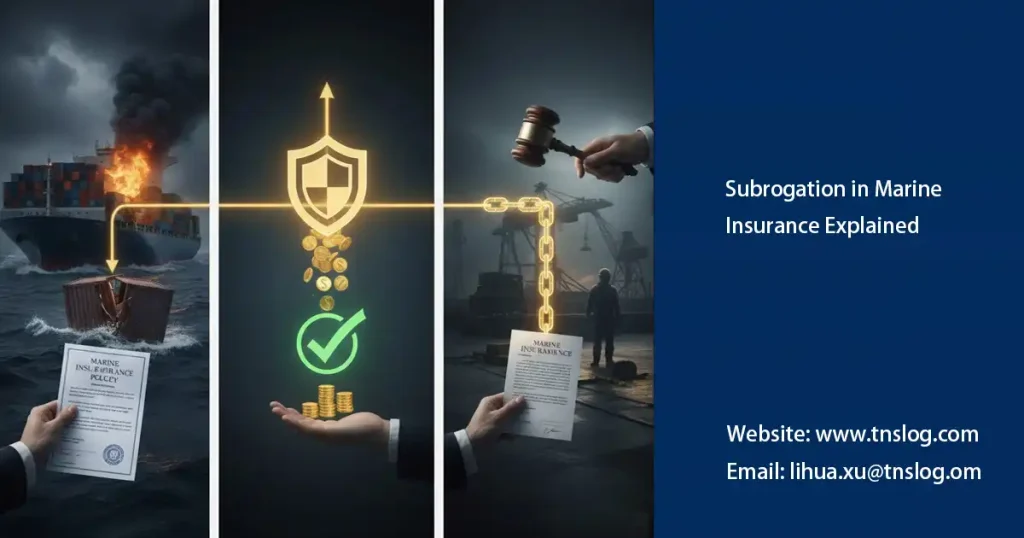

Subrogation in Marine Insurance Explained

Subrogation is a cornerstone of marine insurance practice—yet it’s widely misunderstood by shippers and even some cargo insurers. This article explains what subrogation is, when it applies, and what it means for both shippers and insurers. You’ll find practical steps to protect your interests, real-world examples, and clear actions to take if you’re involved in a claim. Written from the viewpoint of a Malaysia-based freight forwarder, this is a practical guide you can use today.

What Is Subrogation?

Subrogation is the legal right that allows an insurer, after paying an insured’s loss, to step into the insured’s shoes and pursue recovery from the party that caused that loss (for example, a negligent carrier, stevedore, or manufacturer). In plain terms:

-

The insurer pays the insured for a covered loss;

-

The insurer then has the right to recover that amount from the responsible third party;

-

The insured cannot obtain double recovery (i.e., be paid by both insurer and the party at fault).

Key elements:

-

Indemnity principle: Insurance restores, not enriches. Subrogation protects this principle by preventing the insured from keeping both the insurance payout and a recovery from a third party.

-

Legal title: After payment, the insurer acquires a legal right (or assignment) to pursue the responsible party.

-

Preservation of rights: The insured must not prejudice the insurer’s later right of recovery (e.g., by settling with the carrier without insurer consent).

When Does Subrogation Apply?

Subrogation typically arises in these scenarios:

Paid Insurance Claim

After the insurer compensates the shipper for cargo damage or loss covered by the policy, the insurer will investigate if a third party caused the loss. If so, the insurer will pursue that third party for reimbursement (subrogation).Third-Party Liability Exists

The likely candidates include carriers, port operators, terminal handlers, freight forwarders (if negligent), or manufacturers. Proving negligence or breach of duty is usually required for a successful recovery.Contractual & Statutory Constraints

Some bills of lading or contracts limit or exclude third-party liability, or international conventions (e.g., Hague-Visby Rules, Hamburg Rules) cap carrier liability. These limitations affect the subrogation exercise and potential recovery amount.Timing and Notice Requirements

Subrogation rights can be lost if the insured waives them (for example, by inadvertently releasing the carrier from liability) or fails to preserve evidence or provide required notices. Prompt notification of loss and preservation of evidence are therefore essential.

Practical red flags:

-

Do not sign unconditional release documents from carriers before consulting your insurer.

Avoid settling directly with carriers without insurer knowledge—this may impair subrogation.

Implications for Shippers and Insurers

For Shippers

You may be required to cooperate: After a paid claim, insurers will expect full cooperation in providing documents, statements, and evidence to pursue the party at fault.

Avoid prejudicing recovery: Any actions that prejudice the insurer’s right to sue (e.g., disposing of damaged goods, admitting liability, or entering settlements without consent) can reduce or invalidate both insurer recovery and the shipper’s indemnity position.

Potential holdback or recovery actions: If insurer recovers from a third party, the insurer keeps the recovered sums up to the amount paid. If the insured had a deductible, the insured may be reimbursed for deductible only if the insurer’s subrogation recovers that portion and policy terms allow.

For Insurers

Right to preserve market fairness: Subrogation prevents moral hazard and keeps premium levels sustainable by putting loss responsibility on the negligent party.

Operational considerations: Insurers run subrogation investigations, appoint legal counsel, and may work with local agents or adjusters. Subrogation can be complex across jurisdictions, increasing cost and time.

Limits due to carrier shields: Where carriers enjoy statutory caps or contractual limits, insurer recovery may be partial. Insurers evaluate the cost-benefit before pursuing marginal recoveries.

Mutual concerns

Documentation is decisive: Bills of lading, survey reports, packing lists, container status photos, and communications are the evidence insurers use to establish third-party liability.

Timing: Statutes of limitation and contractual notice windows apply—delays can kill subrogation claims.

How to Protect Your Interests (Checklist)

-

Notify insurer promptly of any loss or damage; follow the policy’s notice requirements.

-

Do not sign releases or settle with carriers without insurer consent. If urgent release is necessary (perishables), obtain a written conditionally-worded release that preserves subrogation rights.

-

Preserve evidence: photos, container seals, packing lists, B/L, surveyor reports, and terminal logs.

-

Cooperate fully with insurer investigations and provide requested documentation quickly.

-

Understand contracts: Review bills of lading and service contracts for liability caps or contractual waivers that affect recovery.

-

Consider supplemental protections: Where carrier limits are inadequate, consider cargo insurance with sufficient limits and extensions (e.g., warehouse-to-warehouse cover).

-

Seek professional help: A freight forwarder or insurance broker can coordinate claims and advise on subrogation risk; legal counsel is advisable for complex cross-border recoveries.

Conclusion: How to Protect Your Interests

Subrogation is an essential mechanism that keeps the marine insurance system fair and functional. For shippers, awareness and prudent behavior—timely notification, careful documentation, and avoiding prejudicial settlements—are the best defenses. For insurers, diligent investigation and cost-effective pursuit of recovery protect the broader insurance market.

If you ship from or through Malaysia and want help protecting your cargo and preserving subrogation rights, our freight forwarding team can:

-

review your contracts and bills of lading for liability traps;

-

coordinate insurance notifications and claims handling;

-

preserve evidence and liaise with adjusters to safeguard recovery potential.

Contact us to review a recent claim or to audit your shipping documentation and insurance setup so subrogation works in your favor—not against you.

Have Anything To Ask Us?

Please fill in your email in the form and we’ll get back to assist you soon!