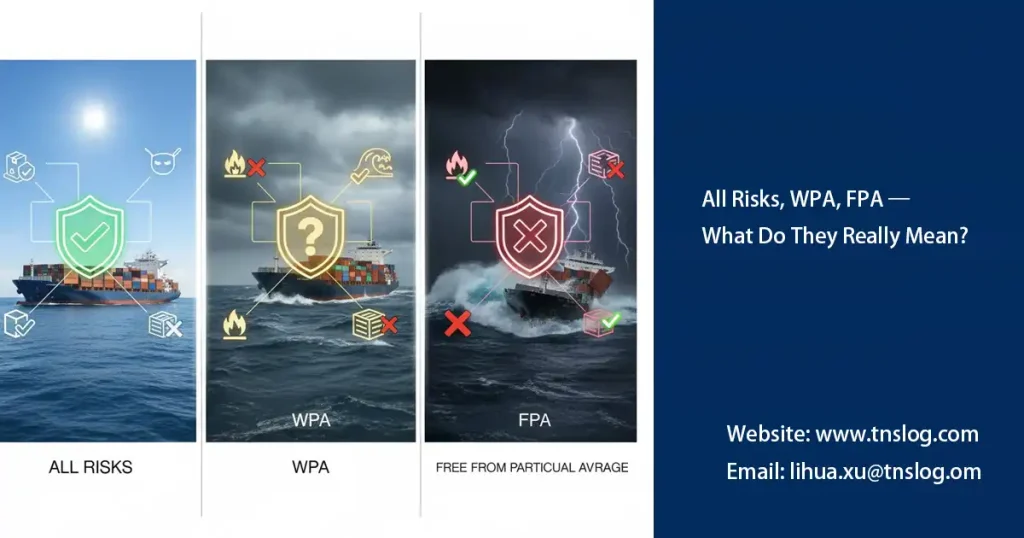

Quick answer: All Risks provides the broadest marine cargo insurance coverage, covering physical losses from external causes during transit but excluding scenarios like improper packing. Opt for this at Port Klang, especially for high-value goods, to simplify the claims process. WPA offers partial coverage for specific maritime accidents, while FPA covers only major losses.

Trusted Marine Insurance Partner

Get Marine Cargo Insurance for Your Shipment from Malaysia

Every shipment deserves the right protection. TNS Logistics Malaysia helps you choose between All Risks, WPA and FPA coverage with full documentation support and dedicated team guidance.