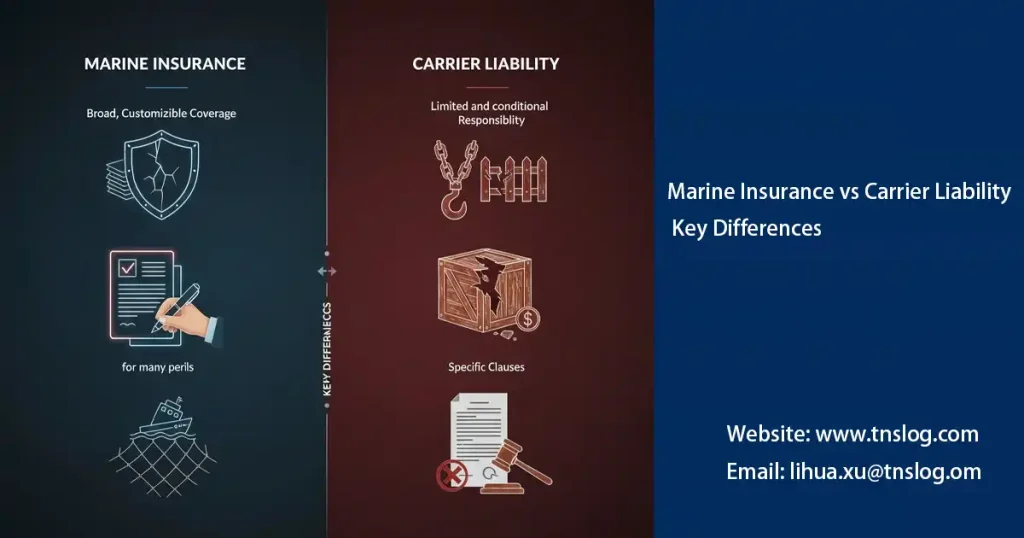

Quick answer: In Malaysia, choosing between marine insurance and carrier liability depends on your shipment's risk profile and exposure. While carrier liability at Port Klang typically covers basic negligence caused damage, marine insurance offers comprehensive coverage against broader risks—including theft and natural disasters—critical for high-value or sensitive cargo.

Frequently Asked Questions

What is the scope of carrier liability at Port Klang?

Carrier liability at Port Klang covers damages during transport due to negligence but excludes acts of God or improper packaging by the shipper.

How does marine insurance benefit Malaysian shippers?

Marine insurance provides broader protection for Malaysia's shippers against risks like theft, collision, and natural disasters, ensuring smoother financial recovery.

Is marine insurance mandatory in Malaysia?

No, marine insurance is voluntary in Malaysia. It’s recommended for high-value cargo or when carrier liability limits are insufficient.

What documents are crucial for claims at Port Klang?

You'll need the Bill of Lading, cargo invoice, and a survey report, among others, for claims related to carrier liability or marine insurance.

Can I extend my marine insurance to cover inland transit in Malaysia?

Yes, many marine insurance policies can be extended to include inland transit or warehousing within Malaysia, covering the end-to-end shipping process.