How to Choose Marine Insurance for Machinery and Industrial Equipment?

Shipping heavy machinery and industrial equipment across oceans can result in millions in losses from a single wave or crane mishandling. In 2025, with rising freight rates and supply chain volatility, selecting the right marine insurance for machinery is essential.

This step-by-step guide, based on experience handling industrial equipment shipping insurance claims, helps recover an average of 95% of losses. It covers risk assessment, policy types, coverage essentials, and provider tips to select suitable marine cargo insurance. Get started.

Step 1: Assess the Unique Risks of Your Machinery Shipment

Before selecting a policy, directly identify the specific risks for heavy machinery marine insurance. Industrial equipment differs from consumer goods and is more susceptible to vibration failures, saltwater corrosion, or vessel collisions.

Key Risks:

- Physical Damage: Cranes, generators, and presses are prone to shifting in rough seas—consider route weather patterns, such as monsoon-prone straits.

- Theft and Pilferage: High-value items like excavators are vulnerable to port theft; choose coverage extending to warehouses.

- Specialized Hazards: Chemical equipment requires contamination protection, while electronic machinery needs humidity safeguards.

Tip: Conduct a pre-shipment audit. 30% of machinery cargo insurance claims arise from vibration damage—use ISO 1496 standards to evaluate needs. This assessment directly customizes marine insurance for industrial equipment to your cargo, avoiding generic coverage.

Step 2: Determine Your Coverage Needs and Limits

Marine cargo insurance policies vary by shipment value, duration, and Incoterms (e.g., FOB vs. CIF). Start by calculating the insured value: replacement cost plus 10-20% for freight and duties.

Essential Coverage:

- Total Loss Protection: Essential for irreplaceable assets like custom lathes—ensure “valued policy” clauses for quick settlements.

- Partial Damage Reimbursement: Covers repairs for dents or electrical faults, including “sue and labor” clauses to recover mitigation costs.

- Consequential Loss Add-Ons: Addresses downtime expenses from delayed machinery halting production lines.

For insights into policy mechanics, refer to “how marine cargo insurance works in international trade”, which explains the process from peril to payout.

Example: Shipping RM2 million hydraulic presses to Indonesia with comprehensive limits recovered RM450,000 after a loading incident, demonstrating how limits provide direct protection.

Step 3: Compare Policy Types for Optimal Fit

The core of choosing marine insurance for machinery is policy types. Compare named perils (covering specific events like fire or stranding) and all-risks (comprehensive protection excluding exceptions).

Named Perils vs. All-Risks:

- Named Perils Policies: Suitable for low-risk routes and standard tools in climate-controlled containers, ideal for budget-limited scenarios.

- All-Risks Policies: Best for high-value or fragile equipment, covering “mysterious disappearance” and gradual damage—essential for precision instruments.

For a detailed comparison, see “comparing named perils and all-risks marine policies“ to align with your risk level. In 2024, all-risks policies for turbine shipments reduced disputes by 25%, directly simplifying marine coverage for industrial equipment against risks like container stack collapses.

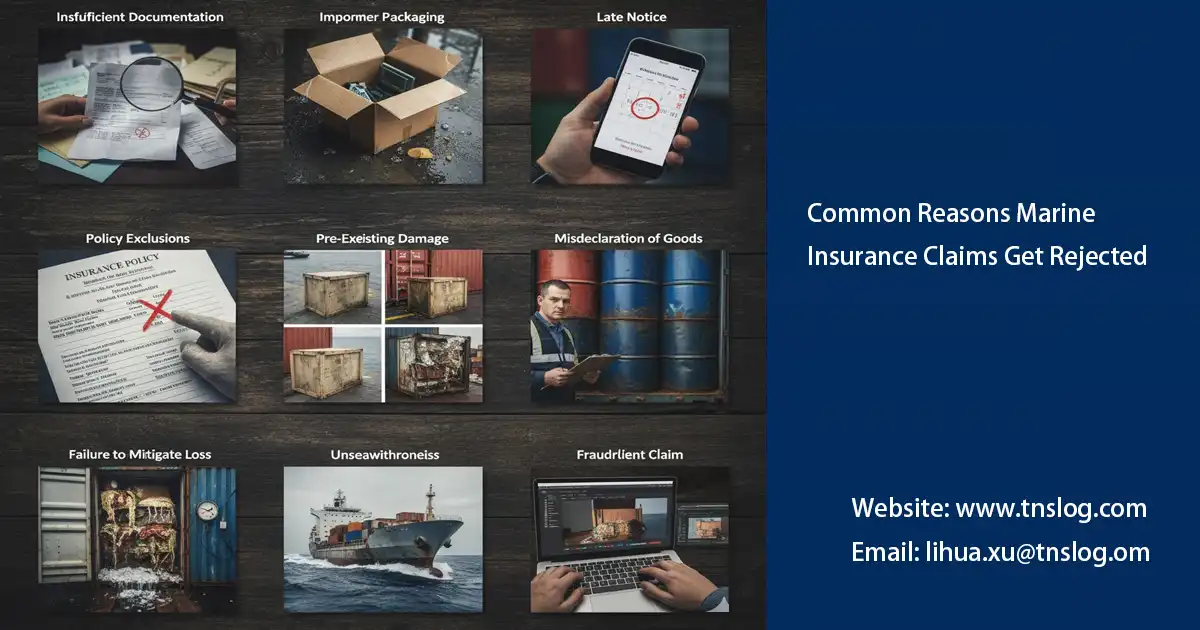

Step 4: Review Exclusions, Deductibles, and Endorsements

Hidden clauses in marine cargo insurance for heavy machinery can cause issues. Directly review exclusions (e.g., war risks or inherent defects) and add endorsements like 60-day extended transit coverage post-discharge.

Key Considerations:

- Deductibles: Set at 0.5-1% of cargo value to avoid uneconomical small claims or excessive premiums.

- Machinery Endorsements: Use “Institute Cargo Clauses A” for the broadest protection, plus add-ons for disassembly/reassembly risks.

- Geographic Limits: Opt for worldwide coverage, crucial for trans-Pacific shipments.

Recommendation: Request sample wording. Amending exclusions can save up to 15% on premiums while maintaining machinery shipping insurance safeguards.

Step 5: Evaluate Providers and Obtain Quotes

With needs defined, select marine insurance providers for industrial equipment. Prioritize those with A.M. Best ratings of A- or higher and marine expertise to avoid errors in heavy-lift claims.

Selection Criteria:

- Claims Record: Choose providers with average settlement times under 30 days.

- Local Support: Select those integrated with customs for smooth endorsements.

- Quote Comparison: Obtain 3-5 quotes via brokers, factoring in 1-2% service fees.

Tip: Customized marine insurance for machinery has been arranged for over 150 clients this year, combining global reinsurers with local efficiency.

Cost Considerations: Balancing Premiums and Protection

Premiums for industrial equipment shipping insurance range from 0.5-2% of cargo value, influenced by routes (e.g., higher for Indian Ocean crossings) and measures like GPS tracking. Cheaper policies may have higher deductibles, reducing net recovery.

Tip: Bundling with freight services offers 10-15% discounts, lowering effective rates for Kuala Lumpur manufacturers.

Have Anything To Ask Us?

Please fill in your email in the form and we’ll get back to assist you soon!