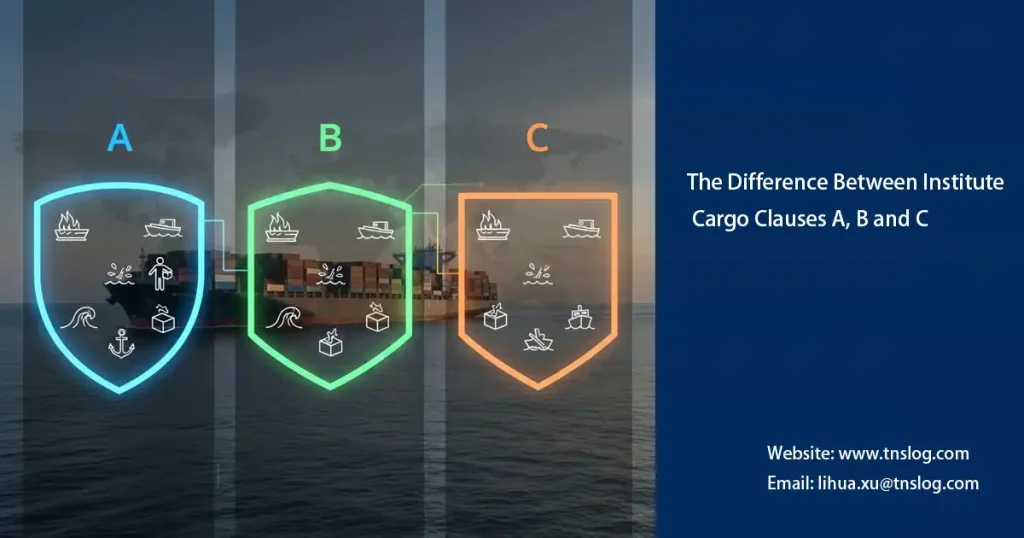

Quick answer: Institute Cargo Clauses A, B, and C differ in coverage and cost. Clause A covers nearly all risks, Clause B focuses on specific named perils, and Clause C targets major catastrophes. For Malaysian exporters navigating routes via Port Klang, selecting the right clause can prevent costly uncovered losses.

Frequently Asked Questions

What risks does Institute Cargo Clause A cover?

Clause A covers all risks of fortuitous loss or damage, excluding war, strikes, or poorly packed goods. It is comprehensive for shipments from Port Klang.

Which clause is best for low-value shipments from Malaysia?

Clause C is the most economical, covering only major events like fire or sinking, ideal for exports where full coverage isn't financially sensible.

How does Clause B differ from Clause A in sea freight coverage?

Clause B covers named perils, such as theft or water damage, whereas Clause A covers all but specified exclusions, making B more selective for Port Klang exporters.

What are typical premiums for Clause A coverage from Malaysia?

Premiums for Clause A usually range from 0.5% to 1.5% of cargo value, higher due to its extensive risk coverage.

Can SME exporters at Port Klang use letters of credit with these clauses?

Yes, but they must ensure Clause A is in place under CIF terms as per Incoterms to comply with financing requirements.